Mainstream blockchains are working toward shorter transaction confirmation times, such as BNB Smart Chain's (BSC) chain's BEP-520 and BEP-525's for shorter block intervals, and Ethereum's research on the pre-confirmation mechanism, etc. These mechanisms directly or indirectly reduce the block time, which has led to a discussion in the community about the impact of these mechanisms on the value of the block. In this blog, we will analyze the impact of block time reduction on the MEV mechanism of atomic arbitrage trading on the BSC chain.

I. Background

With the proposal of BEP-520 and BEP-525, BSC is about to enter an era of 750ms, and shorter transaction confirmation time has become the development goal of BSC, but at the same time, the shortening of block time will bring the validator the concern of MEV value decline. We will analyze the impact of block time shortening on the gain of Atomic Arbitrage on BSC, and the contribution to the MEV value of the block from different perspectives .

II. The impact of block time shortening on the value contribution of Atomic Arbitrage blocks

2.1 What is Atomic Arbitrage

Atomic Arbitrage is a risk-free arbitrage strategy that utilizes the "atomicity" feature of blockchain transactions to simultaneously perform multiple asset exchange operations in a single transaction, thereby capturing price differences between different markets or liquidity pools to achieve risk-free arbitrage.

- Atomicity: In the blockchain, all operations within a single transaction are either fully executed or fully failed and rolled back, without partial success. This ensures the security and certainty of arbitrage transactions.

- Arbitrage: The act of buying low and selling high between different markets using price differences to make a profit on the spread.

An atomic arbitrage strategy therefore encapsulates the multiple steps of arbitrage into a single atomic trade, ensuring that the arbitrage process does not result in losses due to market volatility or trade failure.

Assuming the existence of n trading steps involving the number of tokens and the price , the arbitrage profit is defined as:

where the arbitrage success is conditional:

2.2 Principle of Atomic Arbitrage Contribution to Block Value

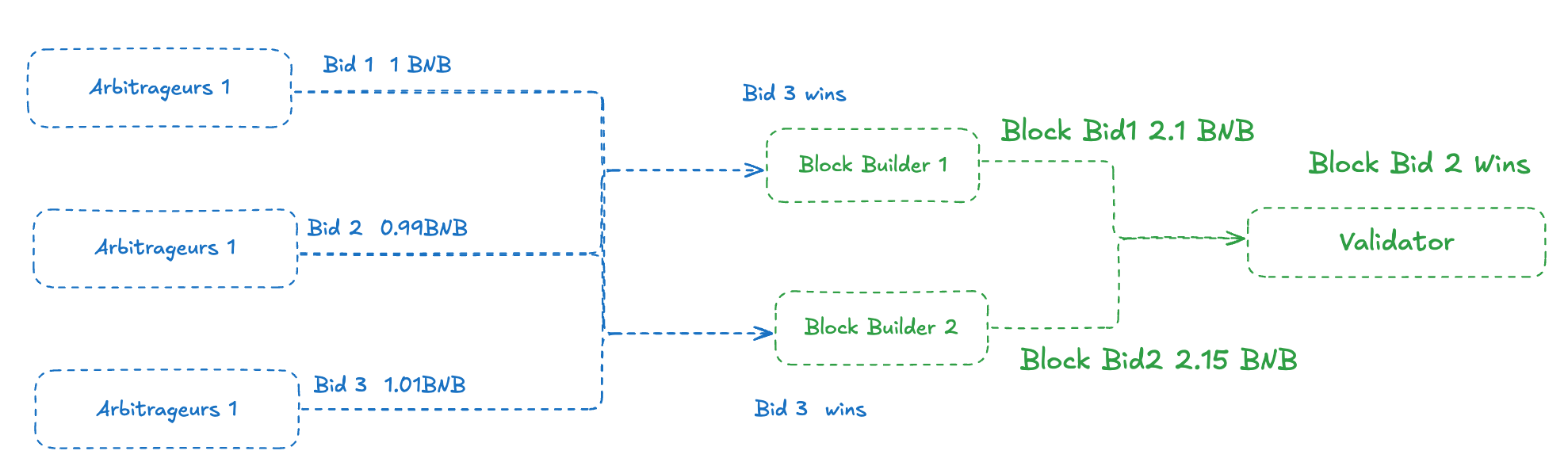

Since the price differences between different markets and liquidity pools are public on the blockchain, for atomic arbitrageurs, they need to obtain arbitrage opportunities in a specific state through public bidding. Under the current PBS architecture of BNB Smart Chain, most of the atomic arbitrage opportunities will be competed at the Block Builder, the atomic arbitrage transaction with the highest bid to the Block Builder will be included in the Block Builder's proposed block, and the block with the highest bid to the Validator will be the block that the Validator proposes.

Due to the nature of open competition, most of the value captured by the atomic arbitrageurs through arbitrage will eventually be submitted to the verifier as additional value of the block. In this paper, we treat the offer cost paid by the arbitrageur to compete for this arbitrage opportunity as the contribution to the block value of this arbitrage transaction.

2.3 Impact of Block Time Reduction on the Transaction Value of Atomic Arbitrage Strategy

In order to quantitatively analyze the impact of block time reduction on the contribution of the atomic arbitrage strategy, we first use data from the BlockRazor Scutum RPC (https://blockrazor.io/#/products/rpc/enterprise )in the 2025 April 15-28 atomic arbitrage transaction value. Atomic Arbitrage trades for the period of April 15-28 are analyzed. The reason for choosing Scutum RPC is that the computational principles and MEV bidding rules of the atomic arbitrage strategy are consistent with the computational principles and bidding rules of Scutum's Backrun Arbitrage, which can be used as a research sample to analyze the contribution of MEV value from atomic arbitrage.

We recorded the quotes and arrival times of all Backrun arbitrage transactions received by Scutum RPC and calculated the difference between their arrival times and the time of the arbitraged trades (signals), which was recorded as Latency (Latency is equivalent to the time spent by the atomic arbitrageurs in receiving arbitrage signals → calculating arbitrage opportunities → issuing arbitrage trades → arriving at the Builder).

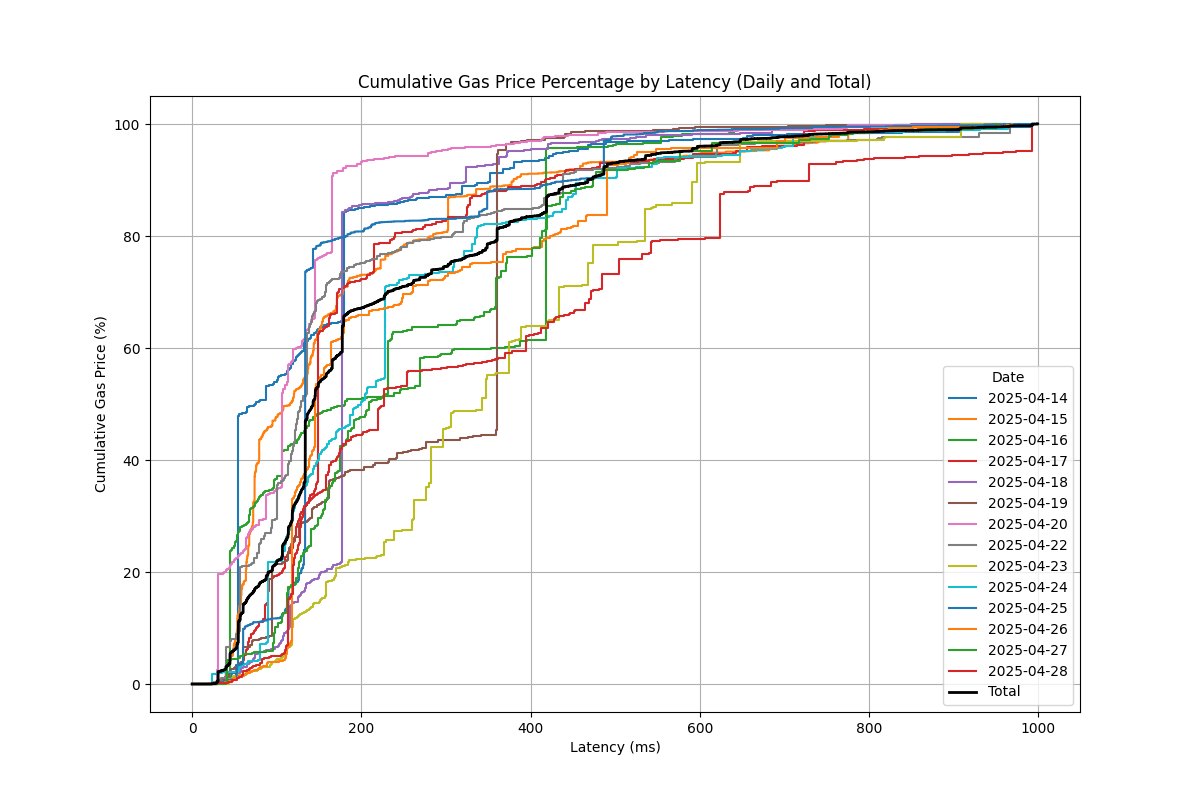

First, we first tagged the Backrun trades of each arbitraged trade (signal), screened the optimal quotes of each signal trade as the latency time grows, summed up the amounts of these quotes, calculated the ratio of the cumulative value of the optimal quotes under the moment to the cumulative value of the final optimal quotes, and finally made the statistics on a daily basis, obtaining the following figure:

It can be seen that as the Latency grows, the total revenue of Backrun transaction is growing gradually, reaching 60% at 200ms and about 99% at about 800ms, and the growth rate slows down significantly with the growth of time.

At the same time, we can see that in the growth curve, there is a more obvious jump in the value volume between 70 - 100 ms and 150-200 ms. We further analyze the transactions with jump in value in this time period, and find that the jump in value comes from the change in the arbitrage path.

2.4 Arbitrage path change rule over time

As mentioned earlier, the profit source of on-chain atomic arbitrage comes from the imbalance between liquidity pools, arbitrageurs calculate the optimal arbitrage path according to different pool spreads, the more tokens involved in arbitrage, the more complex the arbitrage path, the higher the gains that arbitrage can bring, and the relative time required for the calculation will also be longer.

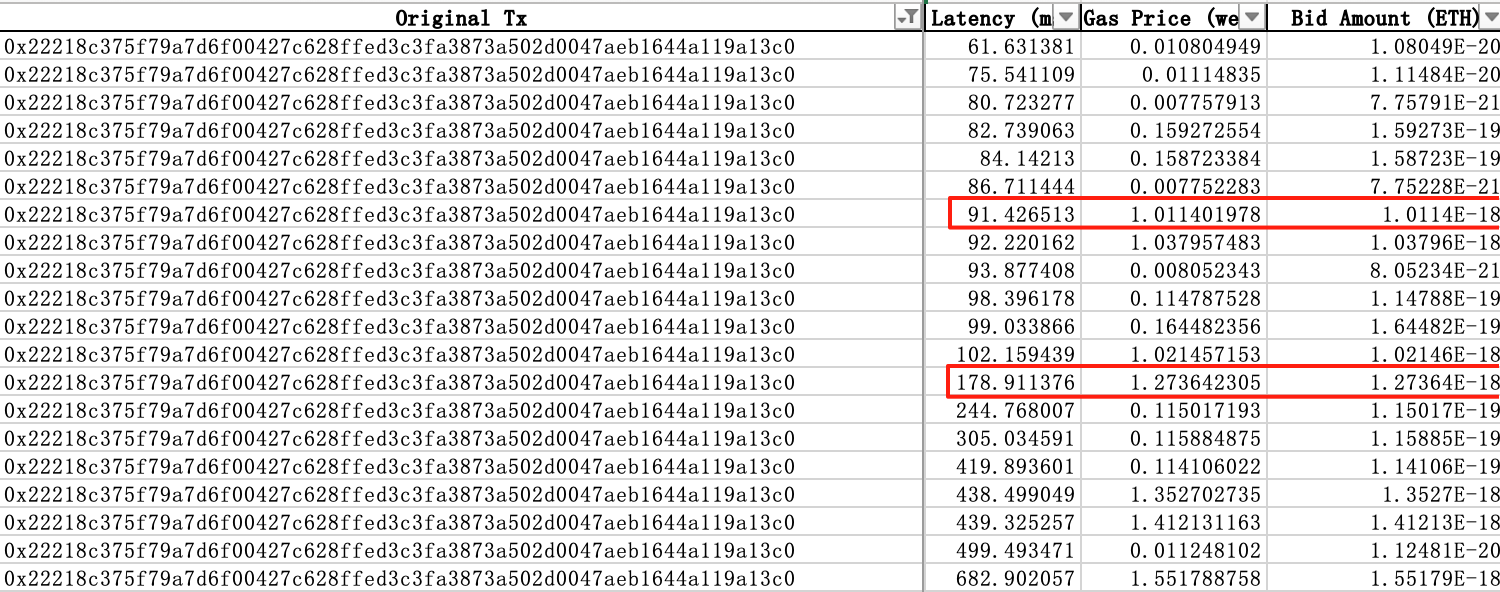

According to our observation, the calculation time for a cross arbitrage using a single currency with different liquidity pool spreads is generally 10 ms, the calculation time for a triangular arbitrage opportunity by adding one more currency to the arbitrage process is at least 70 ms, and the calculation time for a more complex quadrangle arbitrage is at least 150 ms. The calculation time for triangular arbitrage and quadrangle arbitrage is basically the same as that for the time of the value jump. The figure below shows a case where the value jumps due to an increase in arbitrage paths, as documented in Scutum:

From this perspective, the longer the block time, the longer the arbitrageurs are allowed to compute, the more value can be extracted from all atomic arbitrage transactions, and the higher the total amount of atomic arbitrage contributed to the value of the block due to the longer block time and the fuller bidding competition between arbitrageurs.

But does a decrease in block time necessarily result in a decrease in the MEV value of atomic arbitrage transactions?

2.5 The effect of the adequacy of public competition on the MEV value of atomic arbitrage transactions

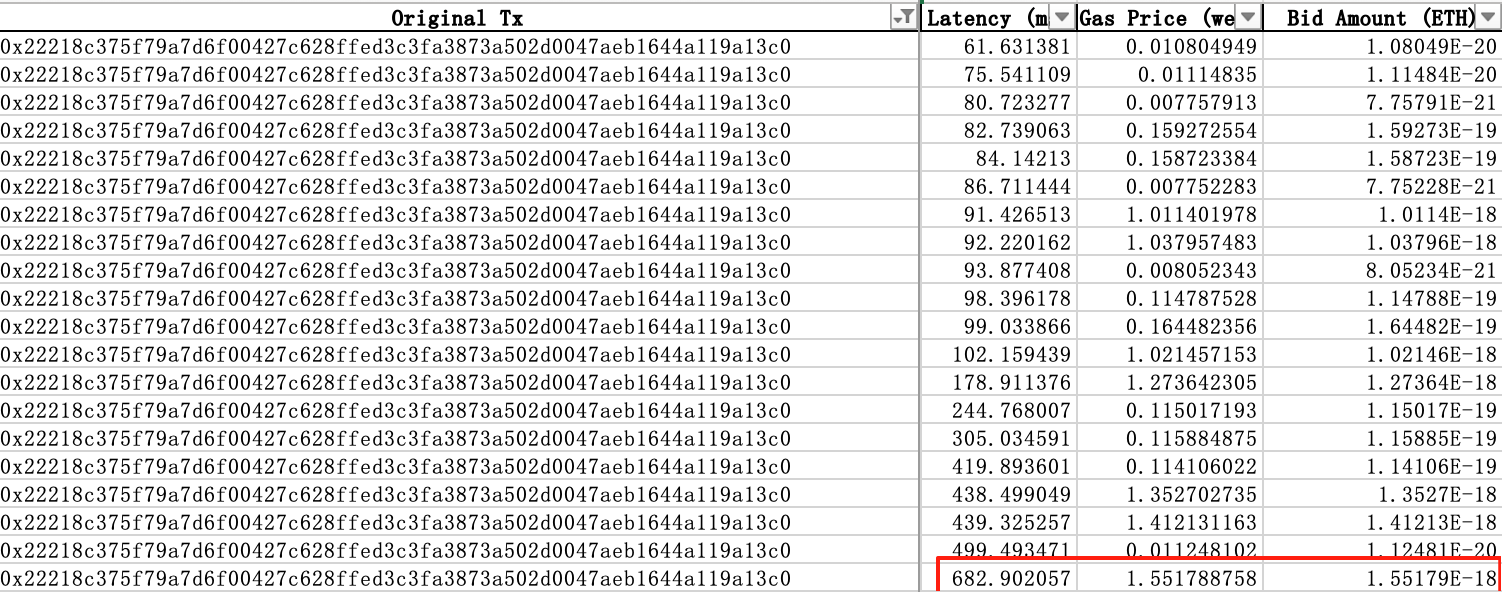

Returning to the graph of Backrun's total offers over time, we find that after 200 ms, there is still a more substantial increase in the block value, and these increases are mainly due to the fact that arbitrageurs will make progressively incremental multiple bids for a particular arbitrage opportunity in addition to the fact that some small, long-tailed arbitrage opportunities are being tapped, and the optimal arbitrage transaction in the case of the jump in the value of the transaction mentioned earlier does not occur until after 682 milliseconds before it occurs.

It can be seen that sufficient competition is significantly helpful for MEV value enhancement, and sufficient bidding will allow atomic arbitrageurs to contribute as much revenue as possible to the block, therefore, the arbitrageur's bid amount as a percentage of his total revenue (bribe ratio) can be a good reflection of the sufficiency of competition.

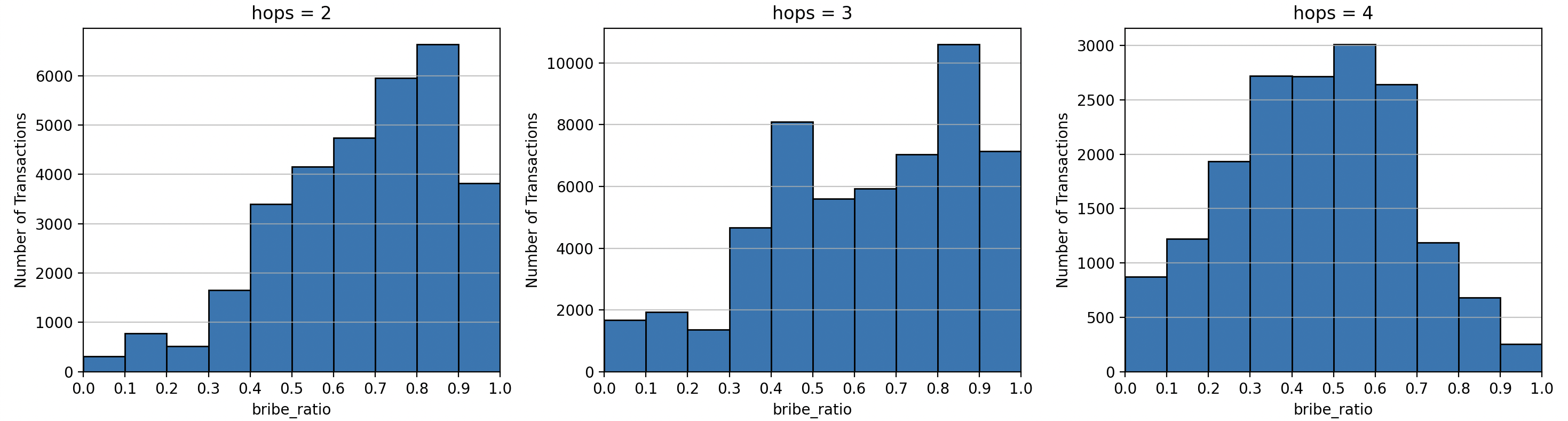

For this purpose, we take the arbitrage trades in the BSC block from May 23 to May 29 and analyze the Searcher's bribe ratio in cross arbitrage, triangular arbitrage and quadrangular arbitrage, and the following is the distribution information of different types of trades, where trades with hops = 2 are cross arbitrage, trades with hops = 3 are triangular arbitrage, trades with hops = 4 trades are arbitrage trades:

The following are the mean and median distributions of the bribe ratio for the different types of trades:

Here is the mean and median distribution of the bribe ratio for different types of trades after filtering out trades with arbitrage gains less than 0.02 BNB.

It can be clearly seen that the bribe ratio of quadrangular arbitrage is lower than that of cross and triangular arbitrage, implying that quadrangular arbitrage is the least competitive.

It also suggests that the quadrangular arbitrage trade taps into the arbitrage value more thoroughly by tapping into more imbalances in the liquidity pool, and so wins open arbitrage competition despite its smaller bribe ratio.

For a given arbitrage opportunity, we assume that the quadrangular arbitrage path Token A → Token B → Token C → Token D → Token A has a total return of and the triangular arbitrage path Token A → Token B → Token C → Token A has a total return of .

However, since the spread of Token C → Token D → Token A is not fully tapped after the execution of the triangular arbitrage, we calculate the remaining arbitrage value record as , which may still be tapped after the execution of the triangular arbitrage trade, and without taking into account the commission discount, .

In the above process, the quadrangular arbitrage for block MEV value is

Triangular arbitrage for block MEV value is

where η is the discount factor, the reason for the existence of the discount factor is that after the execution of the triangular arbitrage transaction, there is a random swap transaction that changes the price state of Token A, C, and D, which affects the arbitrage space, and η is 1 if these two arbitrages can be executed consecutively.

In the current bidding model comparing the value of a single conflicting arbitrage trade, since , even if the quadrangular arbitrage bribe ratio is lower, as long as , the The quadrangular arbitrage trade is also able to win the bid.

However, considering that the residual arbitrage value after triangular arbitrage can still be fully exploited, the only way to maximize the validators‘ return against atomic arbitrage to let the quadrangular arbitrage trade compete fully so that , or to choose the time interval of the block where the triangular arbitrage is fully competing while the frequency of the quadrangular arbitrage is low.

III. Summary and Inspiration

Under the current bidding model, the contribution of atomic arbitrage to the block MEV value increases as the block interval time increases, and reaches its maximum at 1000 ms. The main reason for the rise is that, with the increase in time, arbitrageurs are able to construct more complex arbitrage trades with increased arbitrage profits, while longer block time brings fuller competition, which ultimately increases the overall value of the block.

Next, we observe that the Bribe ratio of quadrangular arbitrage trades is lower compared to cross and triangular arbitrage trades. Since the gains from quadrangular arbitrage can essentially be tapped by multiple triangular or cross arbitrage trades, the frequency of quadrangular arbitrage can be reduced by decreasing the block time, which can instead increase the contribution of atomic arbitrage to the MEV value of the block. .

Therefore, when designing the block interval time, we need to focus on observing the impact of the block interval time on the intensity of the competition between arbitrageurs under the condition of guaranteeing that the arbitrage can operate normally, and promote the full competition between arbitrageurs in order to enhance the contribution of the atomic arbitrage strategy to the value of the block.